I have recently been trying to support a handful of clients, and my employee, Paige, in finding a decent solution for health benefits. If you work for a large company, you are set. But if you work for a small business, the landscape is pretty dreary.

As a finance person, I understand the costs of healthcare. And I understand that it doesn’t just come down to costs, but also the quality of the benefits provided. We are fortunate in this country to have some of the best doctors and hospitals in the world.

Unfortunately, the structure of our healthcare system in the U.S. leads many individuals and families to make important life decisions solely based on healthcare benefits.

For example, in the past, I worked for a large company that offered great benefits, but the culture of the organization sucked the life out of me. In other words, I worked in an environment that literally made me sick so that I could access health benefits. Fast forward starting my business in 2013. While watching my health insurance premiums increase 30-40% per year, my then-boyfriend (now husband) and I used to joke that we should get married so I could go on his health insurance.

And another example: I was speaking with a woman just the other day who said she stayed married to her husband because of the benefits.

Are these healthy choices? Does this lead to a fulfilling life?

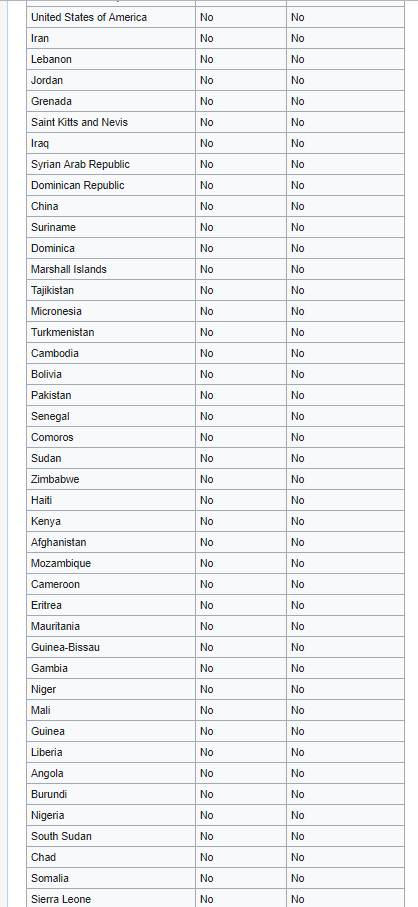

The U.S. is the only country in the developed world to not offer some form of universal or free healthcare. (Universal coverage is not the same as “free.” The common denominator for universal coverage programs is that some form of government action is aimed at extending access to healthcare as widely as possible, as well as setting minimum standards.) As you can see from the list below, we are not in particularly good company.

Countries NOT Offering Universal or Free Healthcare

Source: Wikipedia: List of Countries with Universal Healthcare

Does this mean I am in favor of universal healthcare? Honestly, I am less concerned about how it is implemented (through the government or through private insurance companies) and more interested in the features:

- Insurance being available to all.

- Insurance being used to cover catastrophic events with a maximum out of pocket set per year based on income level.

- Everyone pays something for their benefits, again based on income.

- And if someone doesn’t have income, then Medicaid kicks in – but with a stronger accountability model than what’s in place today.

Again, I don’t have a strong view for how this should be done, but not having access to healthcare may be making our communities sicker, not healthier.

Off my soapbox… and onto QSEHRA

As a small business owner, not being able to offer benefits means that it can be tough to compete for talent. For example, I almost lost Paige to Merrill Lynch because of their benefits package!

As a Certified B Corp, I feel a great responsibility to our clients, our community… and to our employees. Not being able to offer Paige some form of benefit has really weighed on me.

Last week, I found at least a partial solution when doing research on behalf of clients and our own company. Thanks to Michael Kitces, a wonderful resource to the financial planning community, I learned about QSEHRAs.

The 21st Century Cures Act, signed into law by former President Obama in late 2016, created the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA). This allows small businesses (fewer than 50 full time employees) to offer a health reimbursement arrangement (HRA) for its employees.

For 2018, the employer can reimburse workers up to $5,050 per year for single coverage and up to $10,250 for families. The benefits include:

- Employee Reimbursements on a pre-tax basis. Employees select their own insurance plan. Reimbursements can be used to pay the premiums for health insurance purchased on the individual market and to pay for qualified medical expenses.

- Employer Reimbursements are tax deductible for each employee up to the limits outlined above. And importantly, to be able to attract and retain employees!

There are a few limitations:

- Companies with more than 50 employees can’t participate.

- And employees cannot double dip – that is, obtain premium assistance tax credits and employer heath reimbursement dollars.

- QSEHRAs are not available to most small business owners themselves (click here for eligibility information.)

Finding an online platform

We are still researching our options, but Take Command Health appears to be a very good fit. We like their values – they established their company to help individuals and small businesses find solutions in this very challenging healthcare environment. And they know about Certified B Corps, which of course puts a plus sign in their column.

If you want to learn more about QSEHRAs, Take Command Health wrote an eBook that outlines the features, benefits, and participation rules.

It’s not a perfect solution and doesn’t address issues in the country’s healthcare system at large, but QSEHRAs help fill the gap for many small businesses. Paige and I are very excited about setting one up to help cover her insurance costs in 2018. Our hope is that other small businesses and small business employees will be glad to learn about this tool as well.

Be intentional. Be informed.

-Roberta