Meredith Whitney, the famed New York City investment advisor who essentially “called” the financial crisis by highlighting her bearish views on banks in 2007, later said “even a broken clock is right twice a day.” In other words, while her forecast happened to be right, she thought it could just as easily have been wrong. She soon found this out – in 2010, she inaccurately projected the collapse of the municipal bond market.Crystal ball gazing in this business is typically an “iffy” proposition. However, this doesn’t stop the industry from offering a multitude of opinions and views this time of year. We are open to giving our view, but with the caveat that our readers know that we know its limitations!

So, with that said, what do we expect from the markets in 2014?

Momentum – Printer Friendly Version – 201401

As you are all likely aware, the bull ran hard in 2013. Many investment managers failed to embrace it, calling it the “most unloved bull market of all time” – primarily because it was so unexpected. Most kept waiting for a pull-back…one that never materialized, even though there seemed to be a host of reasons why it should.

We have been primarily in a momentum-based market since 2009 – with markets largely being propelled forward by a “friendly Fed” through its Quantitative Easing (QE) program. And so far, the Fed’s policies appear to have had some success in spurring economic growth, and in turn, reducing unemployment.

What could support a continued bull market run?…

- A Fed That Stays Friendly After all the hand wringing, in his final speech as Fed Chair in December, Bernanke announced that QE would only be reduced by $10 billion (from $85B to $75B per month), and that interest rates would likely remain at current low levels into 2015 or beyond. The markets responded as though he had pulled a rabbit out of his hat, with the Dow surging almost 300 points. QE will likely continue to be unwound in 2014, however, Bernanke’s modest step appears to have instilled confidence that the market will likely be able to weather the taper. Meanwhile, short-term interest rates may continue to be held at near historic low levels – which could be a positive for both for the consumer and for the markets.

- The Great Rotation Long-dated Treasury bonds continued their slide in 2013, with the Barclay’s Long Term Treasury Total Return Index losing -12.7%, the second worst performer for the year after gold, which was down a whopping 28.3% . (Gold enthusiasts, who seem convinced that gold would continue its meteoric rise, are likely disappointed – yet another example of why taking a “buy and hold” approach may cause challenges when striving to build wealth.) Though short-term interest rates are currently at a near low, the specter of higher interest rates has pushed yields on longer maturity bonds up—and prices down. This has likely helped spur outflows from bond funds and into stock funds – what has been labeled by many as The Great Rotation—and helped push stock prices up and bond prices down. This phenomenon will likely continue into 2014.

- Stronger Fundamentals Unemployment is falling, and the U.S. economy appears to be improving, which likely bodes well for consumer spending and the market.

What worries us…

- History During most cyclical bull markets, we typically seen a 10+% pull back each year – the equivalent of “letting off a little steam,” so the bull can continue its run. We haven’t had such a pull-back since the fall of 2012! And the current bull may be a little “long in the tooth” – depending on one’s definition, the average bull lasts between 39 – 50 months. As of January 2014, we were entering month 60 of the bull market that began in March 2009.

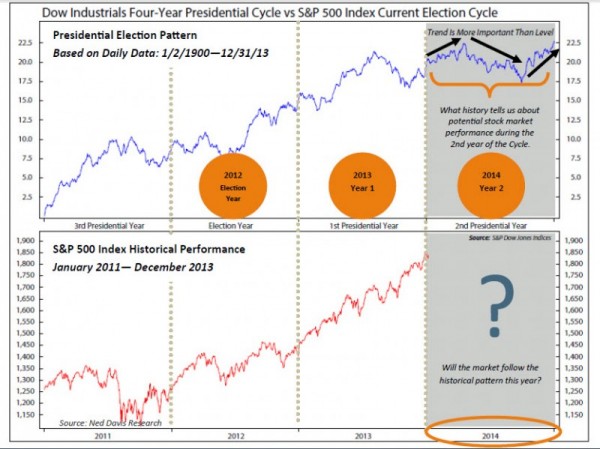

- The Presidential Cycle The Presidential Cycle is one that we watch closely. We have just finished the “post-election year” and are entering “year two,” which has historically been the worst year of the four-year Cycle (see below.) The theory is that when first elected, presidents make promises to try to keep everyone happy, which helps propel the market forward. Then, in year two, they take care of the “dirty work, which often rubs the public in the wrong way, and may contribute to more market volatility. The good news is that the third year of the Cycle is typically fairly good.

- Stock Buy Back Levels Many companies borrowed money in 2013. With limited growth prospects, and interest rates near record lows, rather than using these funds to primarily finance growth, many companies used these funds to buy back their own stock – AKA, “stock buy backs.” As a result, share prices moved up, but not necessarily for all of the right reasons—that is, not necessarily because of increased profitability and better earnings. The amount of buy backs have only surpassed 2013 levels once – in 2007. The question is, is this sustainable? Maybe for a while. The change may come when short-term interest rates finally begin to move up, resulting in companies likely selling their stock back to the investing public to raise cash to pay off the money they borrowed.

- Valuations Value Line’s P/E ratio for the market has been bouncing between 18 and 18.5 over the past quarter, compared to an average of approximately 14.5. Valuations may stay stretched for a long time before the market corrects – but it is likely something to be aware of – money managers are searching for “good deals” and there appears to be very few.

In summary, there will likely be more volatility this year compared to last – and possibly a bear market. However, we will be respectful of the current positive price momentum – striving to stay squarely focused on what the current market price action is doing, rather than what we think it should be doing – and seeking to use the discipline of our models to help guide us.

Live well. Invest well.

– Roberta

Information contained herein is for informational purposes only and is subject to various interpretations and time-frames, and should not be considered investment advice. Advice may only be provided after entering into an advisory agreement with Alexis Advisors, LLC (“Advisor.”) Advisor does not assume any legal liability or responsibility for any incorrect, misleading or altered information contained herein. Advisor shall not be liable for the improper or incomplete transmission of the information contained in this communication. Past performance is not indicative of future results while changes in any assumptions may have a material effect on projected results. Third Party Research Disclaimer: Third party research is provided for information purposes only and has not been prepared by Alexis Advisors, LLC. The information contained herein is based upon sources which we believe to be reliable, but no representation, express or implied, is made with respect to the accuracy, completeness or reliability of the information or opinions in the reports. About: Alexis Advisors, LLC is a Registered Investment Advisor with the Commonwealth of Virginia. Advisor’s current Disclosure Brochure is set forth on Form ADV Part 2 and is available for your review upon request. Please contact Advisor promptly if there are any changes in your financial situation or investment objectives, or if you wish to impose, add or modify any reasonable restrictions to the management of your account.