Regardless of the product under consideration, I think it is usually a good idea to educate yourself about how your money is being invested – hence my first Core Tenet, Be InformedI am frequently asked if annuities are a good retirement planning tool. Of course, the answer is “it depends” – like all aspects of financial planning, it depends on one’s personal circumstances.

Annuities can be particularly confusing, but it’s worth taking the time to understand why you are buying the product, as well as what you are buying – that is, the specific product features.

There are three common types of annuities:

- Fixed annuities generally guarantee a fixed or minimum rate of return over a specific time period. Most reset the rate of return at the end of a pre-determined time-frame. In most instances, a fixed annuity can be compared to buying a CD. Given today’s low interest rates, fixed annuities yields are low, and as a result may be impacted by inflation – that is the dollar amount may stay the same, but the value is eroded by inflation. (Remember the “nickel loaf of bread?” Me neither, but this is an example of inflation – that a nickel doesn’t have the same purchasing power as it did in the past.)

- Variable annuities (VAs) allow premiums to be invested into a limited number of sub-accounts (similar to mutual funds), which may include stock, bonds, and cash. VAs may also offer a guaranteed minimum rate of return, even if the underlying investments underperform.

- Equity Indexed annuities contain features of both fixed and variable annuities, offering investors a return based on a specific benchmark, such as the S&P 500 Index.

On the surface, these products may seem appealing and simple – you pay the insurance company a premium either via lump-sum (typically called an “immediate annuity”) or periodic payments (typically known as a “deferred annuity”). In return, your money grows on a tax-deferred basis, and you may receive a steady stream of payments over time.

Below the surface, however, these products can be complex and may require digging deep to understand the cost versus potential benefit.

Ask Questions

The most logical place to start is by asking:

- Why am I buying this product? Is it to move a taxable account into a tax-deferred status? Is it to receive a guaranteed income payment? Other?

- Do I understand the tax implications of moving money into an annuity?

- Is there a surrender period?

- What are my total costs?

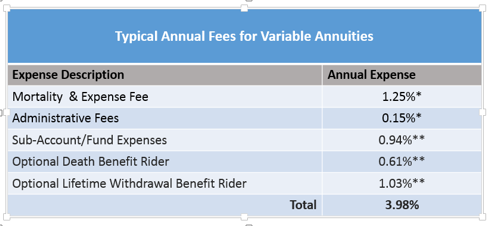

Some annuities can be expensive, depending on the provider and the riders purchased. An example of base VA fees (*), as well as fees associated with riders (**) that may be added on, is displayed below.

As you can see, the costs can add up:

- Mortality & Expense (M&E) Fees Insurance companies charge a fee for assuming the risk of the annuity. These fees may also be part of the commission received by the advisor for selling the annuity.

- Administrative and Operating Fees Account maintenance fees, such as bookkeeping.

- Sub-Account/Fund Expenses Fees associated with the sub-accounts/mutual funds.

- Optional Death Benefit Rider Adding this rider provides a death benefit to the contract holders’ beneficiaries.

- Optional Lifetime Withdrawal Benefit Rider Adding this rider delivers a guaranteed income stream for the remainder of the contract holder’s life.

A final question worth considering is, “How is the risk being managed in the account?” VAs, like most other investment accounts, are subject to the whims of the markets. So, it’s typically a good idea to ask how the risk (volatility) is being managed – and if there are additional fees being charged for these investment advisory services.

Our Offering

As a fee-only Registered Investment Advisor, we strive to be transparent in how we do business. We charge an annual fee for managing client assets, and an hourly fee for financial planning services. We don’t receive any other fees or commissions.

If we think a client may benefit from a VA, we have a solution – one that is transparent, relatively inexpensive and simple to understand. Jefferson National’s VA product costs $140 per year, plus the cost of the sub-account/funds – many of which range between 0.75% – 1.00%. There are no riders or other bells and whistles, and as a result, the product is relatively easy to understand, with the primary objective being to move a taxable account into a tax-deferred status. Additionally, Jefferson doesn’t pay commissions to advisors for placing business with them, likely reducing the potential for conflicts of interest.

But even with these seeming advantages, the individual first and foremost needs to ask, “Does this product make sense for my particular situation?”

In closing, we believe all consumers of financial services should be informed. An annuity may be the right product for you – we just suggest that you put a bit of time and effort into understanding the details.

If we can assist, please contact us. We are here to be a resource!

Be well,

Roberta

* / **Source: Ken Fisher: Annuity Insights: Your Guide to Better Understanding Annuities. *Securities & Exchange Commission (SEC), Variable Annuities: What You Need to Know. **Insured Retirement Institute’s 2011 IRI Fact Book

Alexis Advisors, LLC is a Registered Investment Advisor with the Commonwealth of Virginia. Information contained herein is for informational purposes only and is subject to various interpretations and timeframes, and should not be considered investment advice. Please contact Advisor promptly if there are any changes in your financial situation or investment objectives, or if you wish to impose, add or modify any reasonable restrictions to the management of your account. Since the confidentiality of internet email cannot be guaranteed, do not include private or confidential information such as passwords, account numbers, or social security numbers. Additionally, instructions having financial consequences such as trade orders, fund transfers, etc. should not be included in your email communications, as we cannot act on unconfirmed instructions received via email. Nothing in this transmission should be construed as an offer or solicitation to purchase or sell securities. Investments in securities and insurance products are not FDIC insured, not bank guaranteed, and may lose value. Advisor’s current Disclosure Brochure is set forth on Form ADV Part 2 and is available for your review upon request.