The U.S. stock markets have been trading in fairly narrow range since year-end with the S&P 500 Index ranging between approximately 2000 and 2100. Most economic data has been positive, with unemployment continuing to decline – the rate stood at 5.5% as of the last Friday’s report, compared to 6.6% in January 2014 and 8% in January 2013.Additionally, inflation has been nearly non-existent, largely driven by energy prices falling off a cliff. And finally, the Federal Reserve has maintained a cautious stance, choosing not to increase interest rates, and intimating that any near-term increases will likely be incremental.

So, with such a positive landscape of declining unemployment, low inflation and low interest rates, what is keeping the U.S. stock market stuck in third gear?

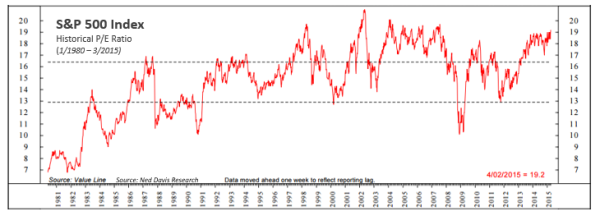

The answer may have to do with rotation – many institutional investors are seeing better deals elsewhere in the world. The U.S. market is relatively expensive, with the price-to-earnings (P/E) ratio of the S&P 500 Index at near record highs, as indicated by the following chart.

Most money managers typically consider relative value when trying to figure out where to invest their money. As Ned Davis Research pointed out recently, “on an aggregate basis, money has been coming out of domestic equity Exchange Traded Funds (ETFs) (-$10.5 billion) since the start of the year and has gone into European ($21 billion) and International funds ex-U.S. ($16.3 billion).”

While it’s tempting to run to your advisor and suggest that s/he over allocate to non-U.S. funds, there is a wrinkle that may be worth considering.

Most mutual funds are priced in U.S. dollars, rather than in their local currency. This means that when the U.S. dollar is going down relative to other currencies, foreign funds tend to benefit. However, the opposite is also true – a stronger U.S. dollar can hurt the performance of international funds.

As you can see from the chart below, which is an ETF that represents the U.S. dollar against a basket of currencies, the dollar has been appreciating since July 2014, largely driven by the expected increase in U.S. interest rates. While this hasn’t precluded international funds completely from appreciating, it has damped the performance.

There are ways around this, however. One approach is to consider a U.S. dollar hedged mutual fund or ETF. Such funds do exactly as their name implies – they hedge the exposure of a rising U.S. dollar, offering a “pure play” on the underlying asset. Again, I suggest speaking with your advisor – and we are always more than happy to assist.

The above is not to say that the U.S. markets can’t or won’t continue higher. Markets can stay extended for months or even years. However, we do think it’s likely worth considering investing in or adding to US dollar hedged international funds as there may be more opportunity overseas for a while.

As always, if you have questions or if we can help in any way, please just send an email or give a call.

Otherwise, until next month.

-Roberta

Alexis Advisors, LLC is a Registered Investment Advisor with the Commonwealth of Virginia. Information contained herein is for informational purposes only and is subject to various interpretations and timeframes, and should not be considered investment advice. Please contact Advisor promptly if there are any changes in your financial situation or investment objectives, or if you wish to impose, add or modify any reasonable restrictions to the management of your account. Since the confidentiality of internet email cannot be guaranteed, do not include private or confidential information such as passwords, account numbers, or social security numbers. Additionally, instructions having financial consequences such as trade orders, fund transfers, etc. should not be included in your email communications, as we cannot act on unconfirmed instructions received via email. Nothing in this transmission should be construed as an offer or solicitation to purchase or sell securities. Investments in securities and insurance products are not FDIC insured, not bank guaranteed, and may lose value. Advisor’s current Disclosure Brochure is set forth on Form ADV Part 2 and is available for your review upon request.