See our f

An optimistic outlook

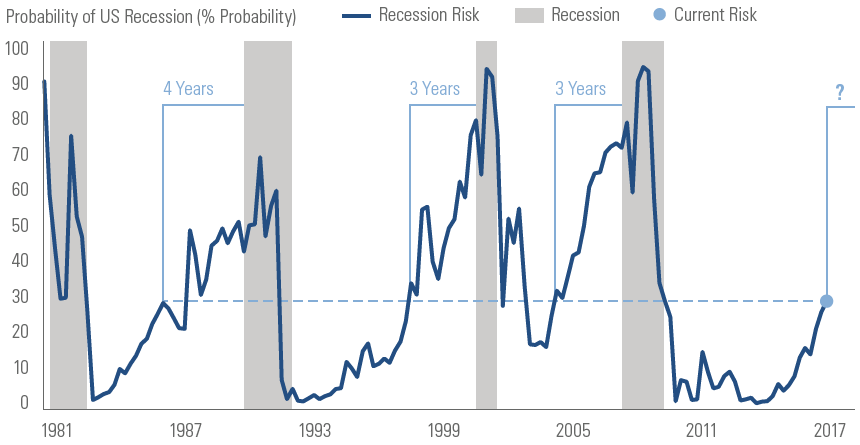

The post-Financial Crisis economic expansion is heading into its 100th month, which puts it squarely in third place for the longest expansion on record. Only the expansions from 1961 to 1969 and 1991 to 2001 are ahead in the race, at 106 and 120 months, respectively.

The market highs and sheer length of time that this expansion has been underway has some investors worried, but economic cycles don’t tend to die simply of old age – as high as the markets may be, there may still be room for them to head higher.

Bear markets typically foreshadow a recession. However, the economists at Goldman Sachs have crunched the numbers and concluded that there is only a 31% chance that the economy will enter a recession within the next two years. This means that there’s more than a two-thirds chance that the current expansion will become the longest ever.

A Rise in Global Synchronicity

Another reason for recent optimism is the increase in global synchronicity. US markets have been doing well in recent years, with international markets much slower to recover from the crisis. However, this divergence is starting to narrow with an uptick in foreign equities – as of the end of Q3 2017, the S&P 500 ETF (SPY) was up just over +15% for the year, compared to the Europe, Australasia & Far East Index ETF (EFA), which is a good international benchmark, up just over +20%. We expect that non-U.S. markets will continue to outperform over the coming months, especially now that European events have started to fade from the headlines.

Divergence slowly narrowing between S&P 500 ETF (SPY) (blue line) and EAFE Index Fund (EFA) (orange line)

US market forecast: Corporate earnings likely to increase

Our readers may remember our analysis of the P/E (or Price to Earnings) ratio over the past months. Yes, the P/E has been high – meaning that stock prices have been considerably higher relative to corporate earnings. In layman’s terms, stock prices (the “P”) have been getting more expensive, without corporate earnings (the “E”) keeping pace. But this trend is starting to level off with corporate earnings improving significantly over the past few months. This is a bullish indicator and bodes well for continued economic expansion.

Tax reform has been foremost on many people’s minds recently. Despite the political gridlock, the expectation is that the new tax legislation, whenever it’s passed, will include lower corporate tax rates. If this turns out to be the case, it could mean more good news for corporate earnings.

Expecting clear skies ahead, with help from Santa

We expect a strong fourth quarter to finish off the year. As of this week, the economy is officially in the “favorable season,” the six-month period that has historically seen the strongest stock market performance most years since 1950.

Another trend to look forward to is what’s festively called the “Santa Claus rally”: a rise in stock prices towards the end of December thanks to year-end trades and the anticipation of additional funds being injected into the market in January.

The main causes for concern right now are continued geopolitical risk with North Korea and policy hiccups in the coming year. Federal Reserve Chairperson Janet Yellen’s term is set to end in four months, and Wall Street is known to dislike uncertainty and change. The big question is whether her replacement will continue her dovish stance on interest rates or take a more hawkish approach and raise rates too sharply. But until then, we expect the ride to continue.

be informed | be intentional